June 1 marks the official start of the 2026 Atlantic Hurricane Season. While experts are cautiously optimistic about market stabilization and a potentially below-normal storm year, the reality for Central Florida residents remains the same: preparation is essential.

At Orca Insurance Group, we’ve seen how the right coverage — and the right partner — provides real peace of mind when storms approach. Here’s what Orlando and Winter Park homeowners and drivers should focus on right now.

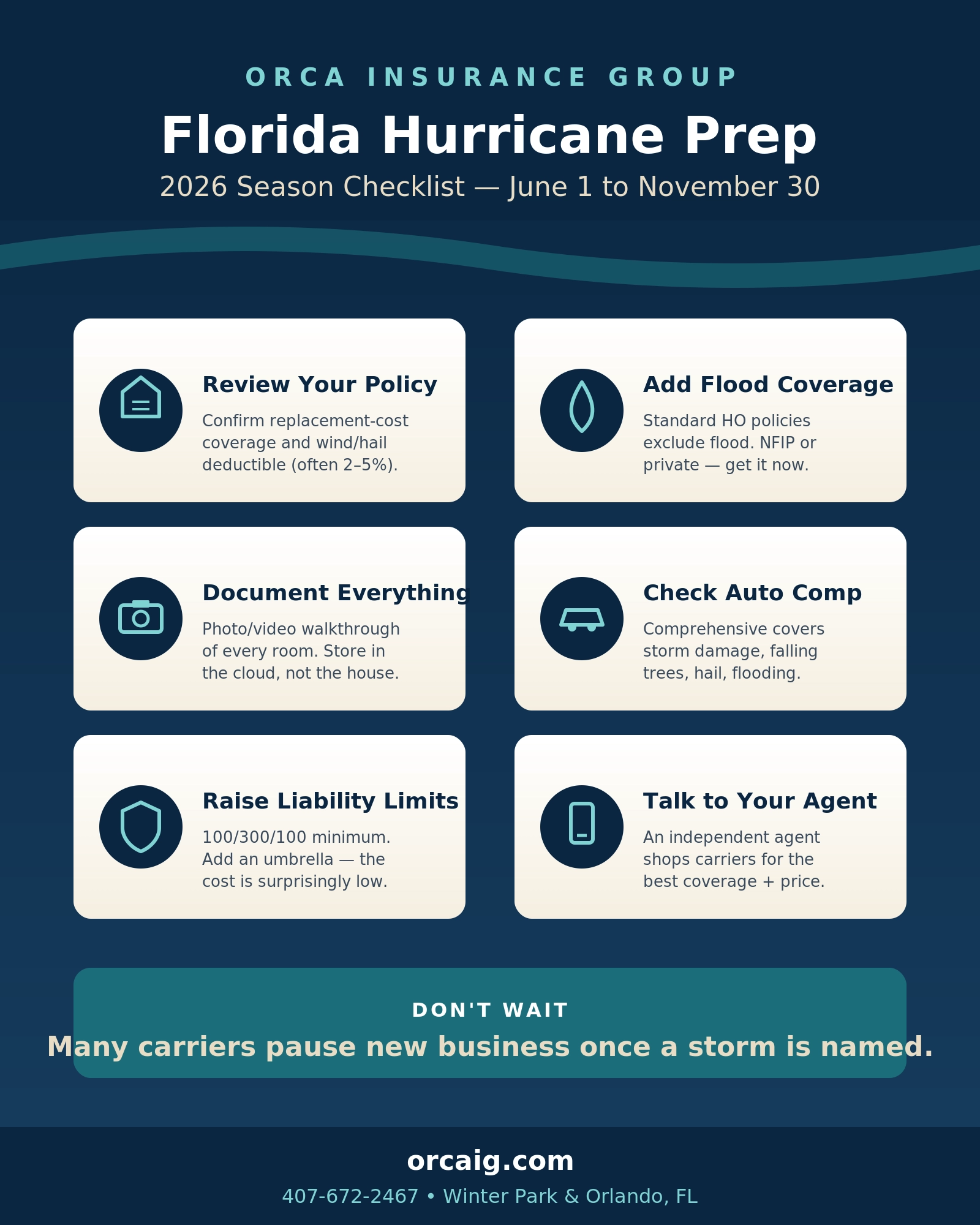

Review Your Homeowners Insurance Before Storms Arrive

Standard homeowners policies in Florida typically cover dwelling (your home structure), personal property (belongings), liability, and additional living expenses if your home becomes uninhabitable. However, they come with important Florida-specific details:

- Hurricane/wind-hail deductibles are often 2–5% of your dwelling coverage (much higher than your standard $1,000–$2,500 deductible).

- Windstorm coverage is included, but understand exactly how your policy applies it.

- Flood damage is never covered by standard homeowners insurance — even from hurricane rains. Separate flood insurance (through NFIP or private markets) is critical, especially in inland areas prone to heavy rainfall flooding.

Action steps:

- Confirm you have replacement cost coverage (not actual cash value) for your home and belongings.

- Check for any available mitigation credits (impact windows, fortified roof, etc.).

- Review your personal property limits — many people are underinsured on contents.

- Ask about bundling your home and auto policies for potential multi-policy discounts of 5–25%.

Start your homeowners insurance review or quote here: orcaig.com/homeowners-insurance or browse our full personal insurance lineup.

Don’t Overlook Your Auto Insurance

Central Florida’s unique risks — heavy I-4 traffic, tourism-related congestion, higher rates of uninsured drivers, and sudden summer storms — make strong auto coverage non-negotiable.

Key coverages to verify:

- Comprehensive (covers storm damage, falling trees, hail, flooding).

- Collision.

- Higher liability limits (we often recommend 100/300/100 or more, plus an umbrella policy for extra protection — the premium difference is often surprisingly small).

- Rental reimbursement and roadside assistance for post-storm mobility.

Florida’s shift away from PIP means bodily injury liability is now even more important. Accidents involving serious injuries can quickly exceed minimum limits.

Review or strengthen your auto coverage: orcaig.com/auto

Why Partner with Orca Insurance Group?

As an independent agency, we shop dozens of carriers to find the best combination of coverage and rate for your specific situation — whether you own a home in Winter Park, rent in Orlando, or need to bundle multiple policies. We understand Central Florida risks intimately and can help you navigate deductibles, endorsements (like sinkhole or mold), and the new claim timelines.

Want to dig deeper into how the market is shifting? Read our companion posts on the Orca blog — including the 2026 Florida market update and the new claim rules every policyholder should know.

Ready to review your full personal insurance portfolio? Call us at 407-672-2467, email [email protected], or start a quote at orcaig.com/personal-insurance.

Don’t wait until a storm is in the Gulf. A quick review now can make all the difference.